Let’s skip the discussion about the the legality of Fractional-reserve banking (at least for now), instead let’s focus on its consequences. Does fractional-reserve banking cause any problems? Does anybody get hurt?

Consider a simple illustration consisting of 4 players: Depositor, Bank, Borrower, and UsedCarDealer.

- Depositor deposits $20K cash into a checking account at Bank.

- Bank lends 90% of Depositor’s deposit to Borrower, who withdraws it ($18K) as cash.

- Borrower takes his cash to a used car lot, sees a used Mustang, and goes over to take a closer look at it.

- Depositor also sees the same Mustang at the same time, goes over to take a closer look at it.

- UsedCarDealer sees 2 people interested in the same car, so he walks over to see if he can close a sale.

- Borrower: “How much?”.

- UsedCarDealer: “$10K. Cash or check, either is fine”.

- Borrower: “That works for me”.

- Depositor: “I’ll give you $11K”.

- Thus an auction commences.

- Depositor can write a check up to $20K.

- Borrower has $18K of cash.

- After several rounds the car is eventually sold to Borrower for $15K, who pays the cash and takes the keys.

From what I can gather, there are 3 problems caused by fractional-reserve banking.

First Problem

The first and most obvious problem is that Bank is in danger of insolvency. Bank only has $2K of cash, so what if Depositor wants to withdraw his $20K balance as cash?

In practice, Bank has many other depositors that aren’t in the same scenario, so the 10% of their deposits that Bank holds will cover the extra $18K. Bank also has the ability to quickly borrow from other banks if needed. If Bank had no other depositors, and could not rely on borrowing, they would not have lent out 90%, because banks are not run by dummies. And finally, deposits are insured by the FDIC so even if Bank is run by dummies, the worst that could happen is Bank will go out of business, but Bank’s account holders will not lose any money as their accounts will be transferred to another bank.

But do these things solve the problem? They mitigate the problem, but do not completely solve it.

The FDIC is funded by the banks, so to make up for it the banks pass that cost on to their customers, usually in the form of higher interest rates for borrowers, less interest paid to depositors, and higher overdraft fees. And it is still somewhat painful for Bank’s account holders to be transferred to another bank, even if they don’t lose any money. And we’ve yet to see what happens when the FDIC runs out of funds.

Second Problem

To understand the 2nd problem, we have to look at what happened to the price of the Mustang. It went up by 50% (assuming UsedCarDealer was correct at placing his original price at $10K). Imagine UsedCarDealer getting a 2nd Mustang, the price he would now expect is around $15K, not $10K, so a person showing up with $12K of cash would have been fine just a few days ago, but is now priced out of the market.

Now imagine an entire economy transitioning from cash-only (or gold-only or silver-only) transactions, to checks drawn on fractional-reserve banks. There would be an enormous leap in prices because the banks alter the money supply. In our illustration Bank created $18K, not by printing cash, but simply by double-entry bookkeeping (i.e. out of thin air). There is now more money chasing the same goods and services, which puts an upward force on the prices – inflation.

As economists have pointed out, inflation hurts the lower classes more so than the upper classes. Even if all prices rise, wages included, they don’t rise at the same time. The lower classes see their costs going up sooner, then their wages come up some time later**. Imagine being one of the first borrowers from one of the first fractional-reserve banks, you get to buy goods and services at their old prices because the merchants will not yet know to raise the prices until they see sufficient buying activity. You saw this whole thing coming because you were in the upper crust and tipped off ahead of time. Now imagine being the working-class guy who has been saving up cash for years to buy a used Mustang – the price went up while you were saving up cash, so you will have to spend a few more years saving up more cash. So the rich get richer and the poor get poorer.

In my understanding, this is a one-time problem that eventually stops. Once an economy fully transitions from cash-only (or gold-only or silver-only) to checks drawn on fractional-reserve banks, the upward force on the price of a used Mustang will reach an equilibrium and stop going up.

Third Problem

The 3rd problem is the hardest to explain, so I’m going to leave out concepts such as interest rates, business cycles, recessions and insurance, and just focus on what happens if there is crop failure. Imagine that the 4 players in the illustration are in a town surrounded by farmland, and about once every 4 or 5 years there is sufficient crop failure to cause some of those who would buy a used Mustang to not have enough money to afford it (remember we are ignoring insurance to keep this simple).

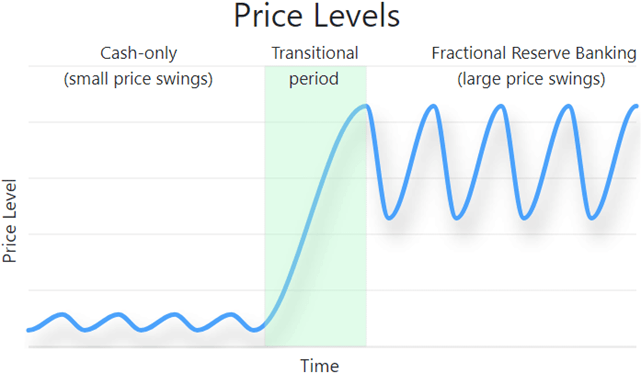

In a cash-only economy (i.e. before transitioning to fractional-reserve banking), the price of used Mustangs would fall somewhat during a year of crop failure due to decreased demand, and rise back to ordinary levels after the crops recovered (assuming the supply of used Mustangs doesn’t change). But in an economy that has fully transitioned to fractional-reserve banking, the price of used Mustangs will swing much more wildly. The chart below shows the simplified general pattern.

We saw above how banks can alter the money supply by creating money out of thin air. By the same mechanism working in reverse, banks can destroy the money they previously created. Banks create money when times are good, and they destroy money when times are bad. To understand this, imagine Depositor as a farmer. He deposits more money in Bank when he sells lots of crops, and Bank responds by creating more money out of thin air and lending it out. But when crop failure occurs, he has to withdraw money from Bank to cover basic expenses (food and rent), and Bank responds by destroying money back into thin air, and reducing outstanding loans. Thus the normal, small price swings are amplified.

Does anybody get hurt? Here I’m taking a page out of George Gilder’s excellent book “The Scandal of Money”. Prices are the signals that entrepreneurs look at when determining how to deploy resources. If an entrepreneur sees that prices are high in a certain market, he may raise money from investors and build a factory to manufacture that product. But if the prices swing low while the factory is still being built, the endeavor is more likely to fail. Price swings introduce noise into the signals that entrepreneurs look at. If the entrepreneur had clear signals, he may have seen that the real opportunity was elsewhere. The larger the price swings, the more noise. The more noise, the more malinvestment. Malinvestment doesn’t just hurt the investors and the entrepreneur, it hurts the broader economy because the broader economy stands to benefit from entrepreneurs succeeding (more products, more jobs, more tax revenue for the government, more donations to charity).

Solution

Murray Rothbard believed that putting the U.S. dollar back on the gold standard is not enough to fix the U.S. banking system, you have to also eliminate fractional-reserve banking.

It is difficult to envision the government doing either of these. But we do have a moral imperative to fix the banking system. And we can fix it. And we don’t need government to do anything at all.

**Copper conducts heat, so when you apply a soldering iron to a printed circuit board the heat will spread out across the board. If you put your finger in the right place, you can feel the speed of the heat’s movement down the copper traces. Fun stuff, and safer than playing with fire. But the whole board doesn’t heat up all at once, the laws of physics prevent it. See Cantillon Effect.

Leave a comment